Drilling ops with Transocean rig pushed forward: New operator taking the helm at Australian gas field

What happened

Amplitude Energy has signed an SPA to buy a 50% interest in VIC/L35 (Artisan) and intends to develop Artisan via tie‑in to its existing Otway Basin infrastructure. The company points to an integrated approval path and is planning development tie‑ins aligned with ECSP work, making a 2028 execution window operationally relevant. Watch whether the planned follow‑on approvals and FID timing firm up and how suppliers respond to the clearer mobilisation horizon

Buyer takeaway

This is a concrete demand signal for tie‑in and subsea execution; procurement should treat the planned tie‑in window as a near‑term scheduling constraint rather than a distant option

Cost / money

Costs shift to the new operator for execution and the royalty structure changes long‑term economics; buyers must budget for mobilisation and execution capex under the new owner rather than assuming seller funding

Supplier / commercial

Clearer timing gives suppliers leverage to shorten quote validity and seek mobilisation deposits; expect pushback on long‑price holds unless contractually defined

Safety / operations

Integration into live pipeline systems raises uptime and handover dependency; include explicit FAT, commissioning and safety acceptance criteria in scopes

What to watch

Watch whether approvals and FID timing firm up and whether suppliers start tightening commercial terms around mobilisation and availability

Key facts

- 50% stake acquired in VIC/L35 (Artisan) under an SPA

- Development concepts involve tie‑in to existing Otway infrastructure with planning aligned to

- Deal includes an upfront cash consideration and a capped royalty over future production

Source excerpts

Jane Norman, Managing Director and CEO, commented: “Producing Artisan through Amplitude Energy’s existing infrastructure allows faster and lower-cost development of this gas for the east coast domestic market. “Artisan development costs will significantly benefit from leveraging the existing ECSP program and our readily-available infrastructure

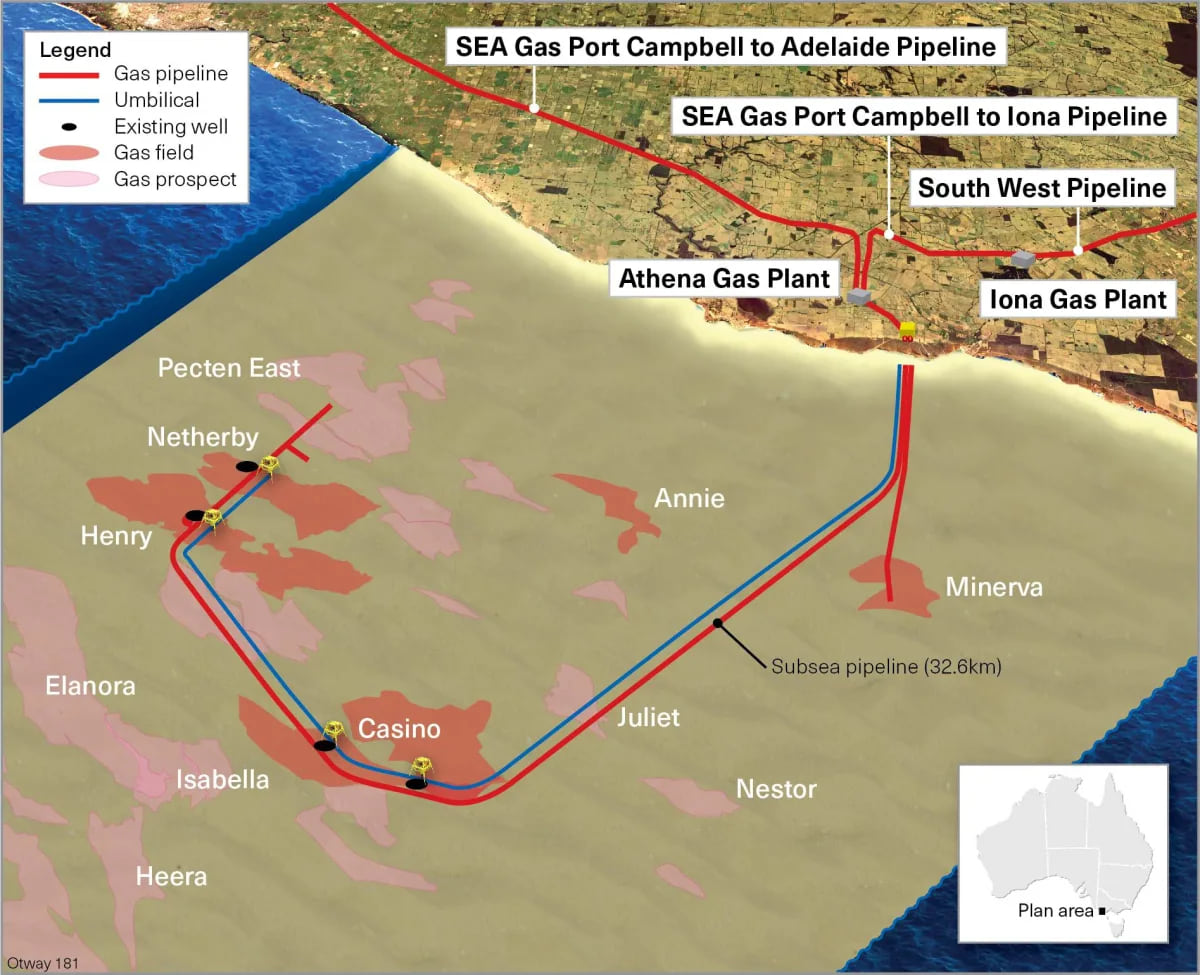

” The development concepts, which are being progressed, involve the tie-in of Artisan to Amplitude Energy’s existing Otway Basin infrastructure in 2028, in conjunction with the development phase of the ECSP

With the primary offshore approvals and licenses for Artisan in place, project-level approvals for the development of the field through the Australian player’s infrastructure will be integrated with other ECSP approvals, subject to a final investment decision (FID). Related Article Amplitude claims that the development of Artisan through its infrastructure allows significant cost advantages due to the proximity to its tie-in to the Casino-Henry-Netherby pipeline