Subsea strategies shift toward tiebacks, standardization and all‑electric systems

What happened

Operators are shifting subsea strategies toward campaign-style tiebacks, standardization and all‑electric architectures to cut cost and shorten cycles. The most important operational detail is the explicit push for earlier contractor engagement and configurable, repeatable equipment that changes tender timing and scope. Watch whether major operators revise RFQs to require modular packages and earlier contractor input

Buyer takeaway

Treat operator preference for tiebacks and standardization as a structural change to RFQ and MSA design: prioritize modular scopes and early contractor pricing gates

Cost / money

Directionally reduces per-project execution costs but shifts some upfront NRE and qualification spending into procurement and tender stages

Supplier / commercial

Firms engaged early gain scheduling priority and may shorten quote validity or insist on deposits for priority capacity

Safety / operations

All-electric and subsea-process variants require revised commissioning and acceptance protocols to ensure safety during handover

What to watch

Watch for operators to adopt contracting models that bundle scope and shorten tender windows; that will favor suppliers already aligned to modular designs

Key facts

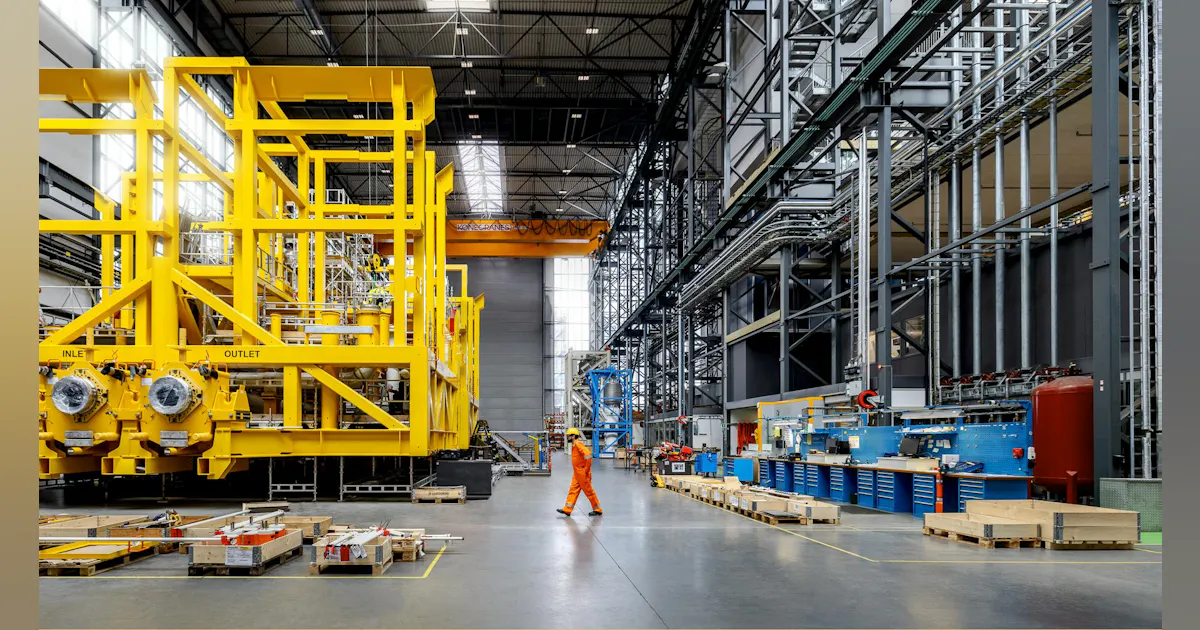

- Operators favour shorter-cycle, campaign-based tiebacks over large greenfield projects

- Standardized, configurable subsea solutions highlighted as major cost and schedule lever

- All-electric and hybrid subsea architectures gaining industry momentum

Source excerpts

Early engagement, standardized and configurable solutions, and commercial models with aligned incentives all make a difference

Offshore: Subsea processing (e

Where do you believe the next meaningful gains in subsea project economics will realistically come from?