Norway gives its blessing for $1.8 billion subsea redevelopment project

What happened

Norway’s regulators approved a large subsea redevelopment project covering previously produced fields, including 11 new wells tied back via shared pipelines. The plan targets first production in the fourth quarter of 2028 and uses multiple subsea templates, making this an operationally meaningful, multi‑template fabrication and installation program. Watch whether follow‑on wells and template scheduling compress yard and vessel windows that APAC projects may compete for

Buyer takeaway

This is a tangible, large subsea workload that will consume specialist fabrication, pipelay and installation windows; treat it as a global capacity factor when planning APAC sequencing

Cost / money

Directional increase in mobilisation and fabrication pass‑through risk as yards and load‑out windows are scheduled; buyers will have less room to push for long quote validity

Supplier / commercial

Expect suppliers to demand shorter quote validity and mobilisation pass‑throughs, and to prioritise customers with immediate sequencing or provisional holds

Safety / operations

Multi‑well tie‑backs raise reliance on ROVs, inspection windows and spares during hook‑up and early production; verify coverage before award

What to watch

Watch whether template fabrication and pipelay bookings overlap APAC project windows — early indications could require provisional holds or sequencing shifts

Key facts

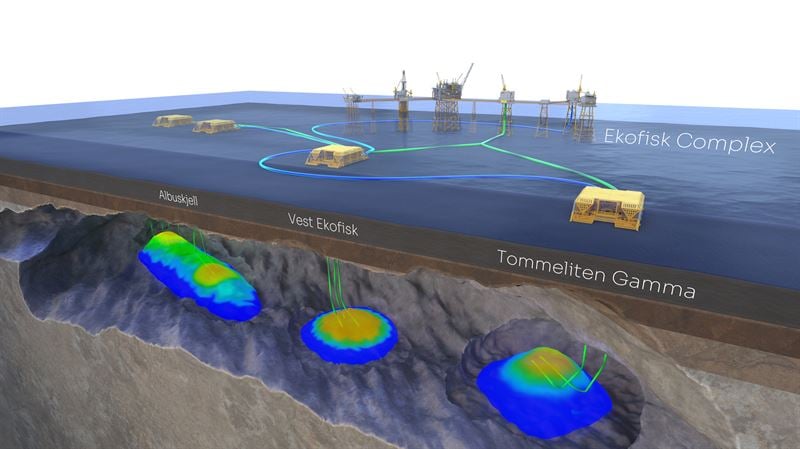

- 11 new wells from multiple subsea templates

- Tied back via a shared pipeline network

- First production planned in the fourth quarter of 2028

Source excerpts

PPF; Source: ConocoPhillips Norway’s Ministry of Energy has approved the plans for development and operation (PDO) for the Previously Produced Fields (PPF) project in the Greater Ekofisk Area (GEA), following a final investment decision (FID) for the redevelopment, which was disclosed in December 2025. ConocoPhillips, which claims that the approval marks an important step in the area’s continued development and supports increased gas deliveries to Europe, operates the project with Vår Energi, Orlen Upstream No

The first production is planned for the fourth quarter of 2028

These fields will be brought back on stream through a subsea development solution tied back to the Ekofisk Complex using existing infrastructure, strengthening gas exports to Europe