Australian offshore production license paving the way for first gas in 2028

What happened

Amplitude Energy received a production licence for the Annie field off Australia, enabling the company to move from planning into field development activities. The licence clears the project to progress toward first gas timing and formal development workstreams, creating realistic sourcing needs for rigs, subsea scopes and local integration. Watch whether permitting and timing hold as the firm aligns detailed EPC and procurement steps

Buyer takeaway

Treat this as a real development timeline: planners should convert tentative requirements into procurement windows and shortlist suppliers now rather than later

Cost / money

Expect shifting spend toward long‑lead items (rig time, subsea equipment, pipeline tie‑ins) which reduces buyer flexibility to delay purchases without schedule risk

Supplier / commercial

Local yards and service suppliers can claim closer commitment and may narrow quote windows or request reservation fees as contracts move from permit to award

Safety / operations

Development pushes readiness tasks (spares, certified crews, permits); failure to align these increases standby and execution risk during commissioning

What to watch

Watch for suppliers to add reservation fees and shorten quote validity once development milestones are published

Key facts

- Production licence granted for VIC/L37 covering the Annie field

- Project now cleared to progress field development activity

- Annie production intended for the east coast domestic market

Source excerpts

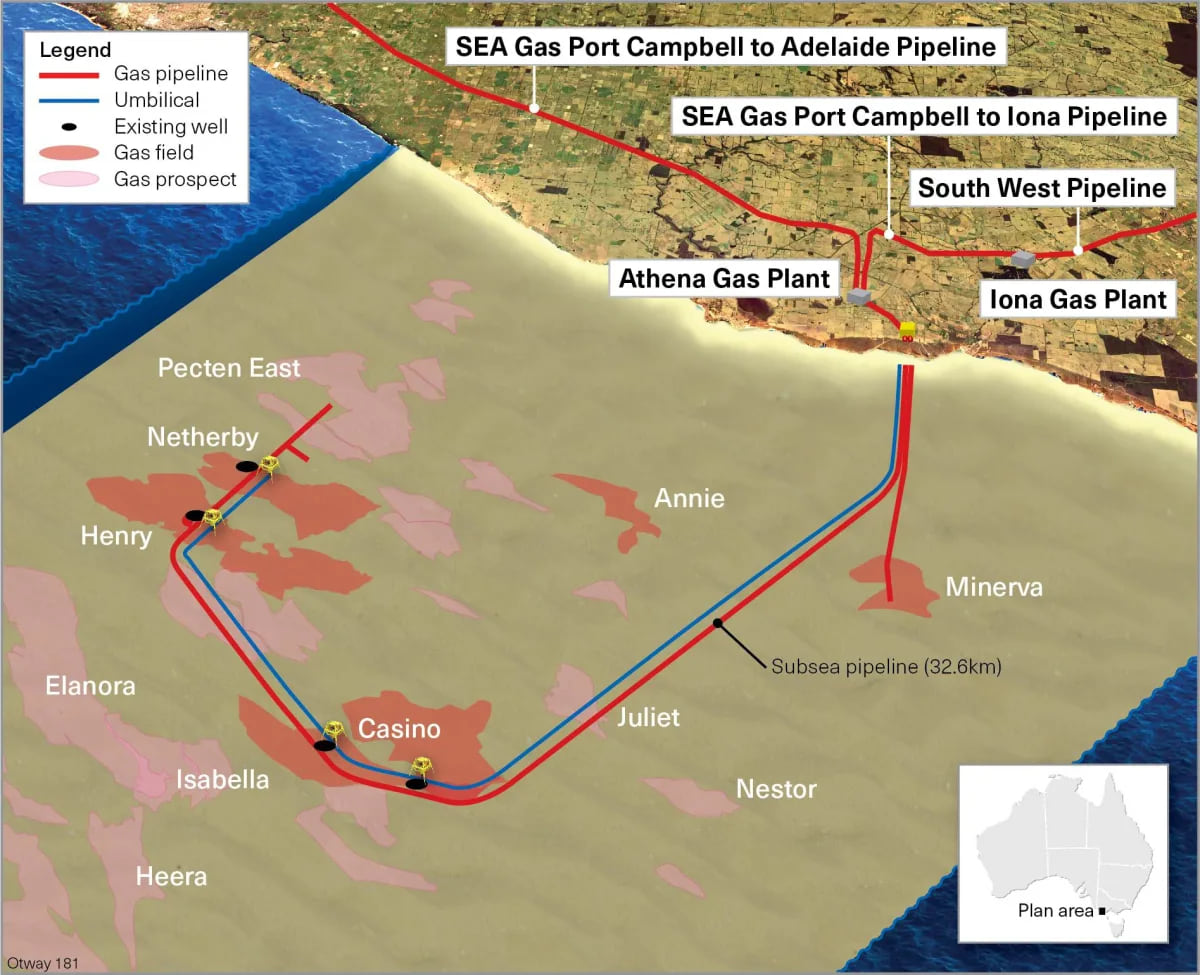

The Australian player holds an extensive portfolio of exploration and development prospects in the Otway and Gippsland basins, including undeveloped discovered resources such as the Annie and Manta gas fields, in proximity to its existing infrastructure

Thanks to this, the firm can move forward with field development activities, with the first gas planned for 2028. “Timely approvals and regulatory certainty for oil & gas projects remain critical given the length of investment cycle required

Otway Basin assets; Source: Amplitude Energy Amplitude Energy has received a production licence, VIC/L37, which covers the Annie field that was first discovered in 2019. Thanks to this, the firm can move forward with field development activities, with the first gas planned for 2028