Europe, Asia LNG prices climb on Hormuz closure

What happened

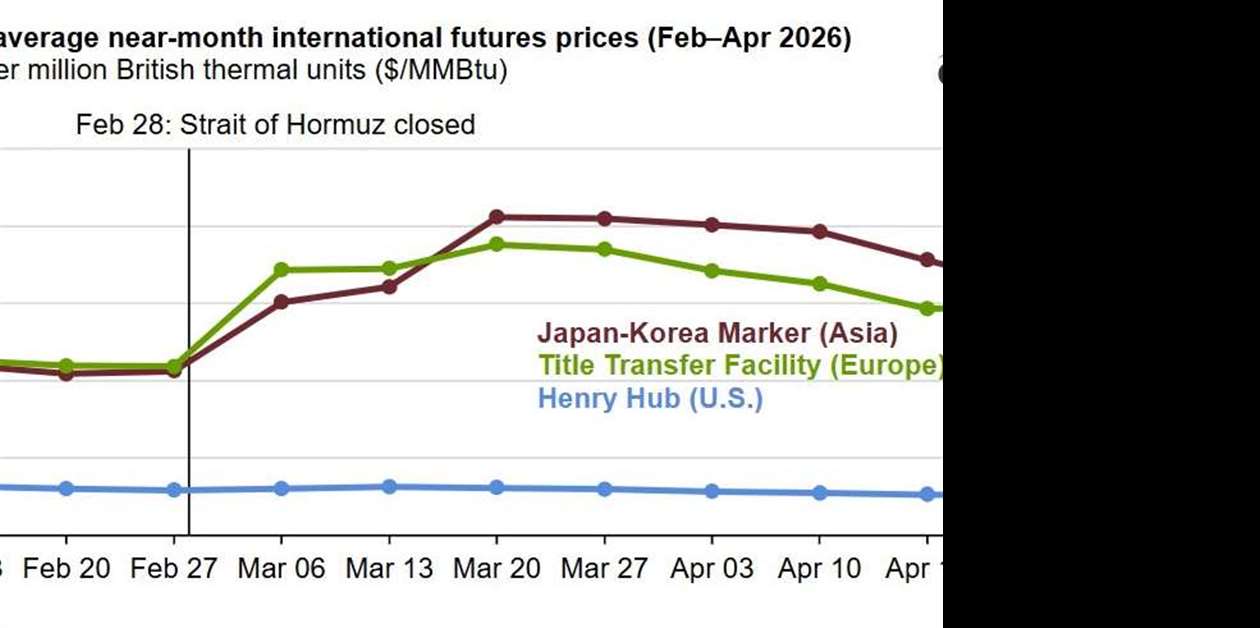

A closure of the Strait of Hormuz disrupted major LNG flows and lifted Europe and Asia benchmark prices sharply. The report notes more than ten billion cubic feet per day of traded LNG was sidelined and that Asian and European buyers scrambled to replace contracted deliveries, which makes spot volatility operationally real for buyers relying on backfill cargoes. Watch whether replacement loadings, route reopenings, or owner contract extensions restore normal flows or if repeated volatility forces more long‑term booking

Buyer takeaway

Treat this as a confirmed supply‑chain shock that raises pass‑through and mobilization risk; adjust sourcing and contract language accordingly

Cost / money

Higher regional spot prices increase potential fuel and freight pass‑through exposure in service agreements and LTSAs

Supplier / commercial

Sellers and shipowners can justify shorter quote windows and accelerated mobilization or deposit terms when cargo flows and freight markets swing

Safety / operations

Compressed shipping and reroutes increase coordination risk at port handover and commissioning; ensure FAT and handover scopes are explicit

What to watch

Watch whether buyers must fill schedules with spot cargoes or can secure long‑term carriage to avoid repeat shocks

Key facts

- More than 10 Bcf/d of traded LNG sidelined according to the report

- No laden LNG tankers crossed the strait between March 1 and April 24

- European and Asian benchmarks rose sharply versus U.S. prices

Source excerpts

Disruption to LNG flows through the Strait of Hormuz has driven a sharp divergence in global natural gas pricing, lifting benchmark gas prices in Europe and Asia while leaving U

4 Bcf/d of DOE-authorized export capacity projected to come online between April and December through Golden Pass LNG Trains 1 and 2 and Corpus Christi Stage 3 Trains 5 through 7

According to Kpler, no laden LNG tankers crossed the strait between March 1 and April 24, effectively sidelining a major share of Qatari exports and tightening global spot markets. The resulting supply shock has forced buyers in Asia and Europe to compete more aggressively for available spot cargoes